Wednesday, December 28, 2011

Thursday, December 1, 2011

Right Shoulder Formation

Based on The chart :

- IHSG is formatting a right shoulder of a Head and Shoulder Chart Pattern

- Running wave is impulsing for wave 5 with the target is around 23.6% retracement around level 3.964 or a lower high from 3.875

- this pattern occured when the impulse is almost over.

beware for the trend that exhausted

Thursday, November 10, 2011

Prediksi IHSG

Prediksi Koreksi Di C kisaran 3.579 < x < 3.624 setelah itu rally hingga breakout lower high diatas 3.875 <x< 4.025

Monday, November 7, 2011

How to Trade This Headline Driven Stock Market

With all eyes on the unemployment report and Europe, the CME Group’s PR Department nearly created an all out panic with their announcement after the market close on Friday relating to futures maintenance margin. The original statement was vague and I was quite concerned until I checked out the CME Group’s web page and the PR Department sent an update clarifying their position. At this point I think the crisis has been averted, but this is just another reminder that we live in “interesting times.”

Keep in mind that if the CME starts raising margin rates across the board for futures contracts in order to protect themselves stocks and commodities could collapse. Silver recently has is margin rates increased and silver since then dropped 25% in value. So imagine if they raised the rates for more commodities…

Keep in mind that if the CME starts raising margin rates across the board for futures contracts in order to protect themselves stocks and commodities could collapse. Silver recently has is margin rates increased and silver since then dropped 25% in value. So imagine if they raised the rates for more commodities…The current price action in the marketplace pales in comparison to the world’s geopolitical tensions and deteriorating social mood.

In my trading career, I have never seen the price action in the indices react so violently to intraday headlines and rumors. Risk is high and the types of traders profiting from this market are day traders and very short term traders with trades lasting just a couple hours to 24 hours in length. Aggressive trading which small position sizes is all that can be done right now. This is not meant to be investment advice, but more as a function of the market environment in which we find ourselves currently trading within.

Right now it is hard to say where price action in the broader indices heads in the short run. One headline out of Greece or Italy could dramatically alter economic history. In the intermediate term I remain neutral to bearish for a number of reasons. One indicator I follow is the bullish percent index on the S&P 500 which at this point is arguing for lower prices.

The chart below illustrates the S&P 500 Bullish Percent Index:

As can be seen above, the S&P 500 Bullish Percent Index is presently at an overbought status. When looking at the relative strength and full stochastics indicators one would argue that a pullback is warranted. Historically when the S&P 500 Bullish Percent Index is this overbought, a pullback ensues which ultimately sees the S&P 500 Index selloff. The more arduous task is trying to determine just how deep the pullback on the S&P 500 Index might be.

It is critical to point out that while I do believe a pullback is likely, I will not rule out a rally into the holiday season. Much of the near term price action is going to be dictated by headlines coming out of Greece and the rest of Europe. In addition to Greece, Italy is also starting to see increased concern regarding an unsustainable fiscal condition. Depending on how the European Union handles the varying degrees of risk in the near term, we could see price action react violently in either direction.

With the market capable of moving in either direction, I wanted to point out some key price levels which should act as clues regarding potential future price action in the S&P 500. The two key support levels to monitor on the S&P 500 Index are the 1,240 and 1,220 price levels.

The daily chart of the S&P 500 Index below illustrates the price levels:

For bullish traders and investors the key price level to monitor is the recent highs on the S&P 500 around the 1,290 area. The weekly chart below demonstrates why this price level is critical and which overhead levels will offer additional resistance should the recent highs be taken out to the upside.

SP500 Weekly Chart Analysis:

While I am neutral in the intermediate to longer term presently, in the short run I have to lean slightly bearish simply because of the future headline risk and also because a major head and shoulders pattern has been carved out on the hourly chart of the S&P 500 Index. This type of chart pattern is synonymous with bearish price action.

The hourly chart of the S&P 500 Index is shown below:

Right now I remain slightly bearish, but should the head and shoulders pattern fail and/or we begin to see multiple positive reactions to news coming out of Europe a strong rally into the holiday season is likely. Unfortunately all we can do is monitor the key price levels and wait patiently for Mr. Market to tip his hand.

Until we see a breakout in either direction, we could see price action inhabit the 1,220 – 1,290 price range for several weeks before we get any more clarity of future direction. Until I see a breakout, I will remain relatively neutral with a slight short term bias to the downside based on price patterns in the shorter term time frames. This is a tough market to trade in, and I don’t want to get chopped around or do any heavy lifting. I’m going to focus my attention on high probability, low risk trade setups until directional biased trades make more sense.

In closing, I will leave you with the thoughtful muse of the late Texas Congresswoman Barbara Jordan,

“For all of its uncertainty, we cannot flee the future.”

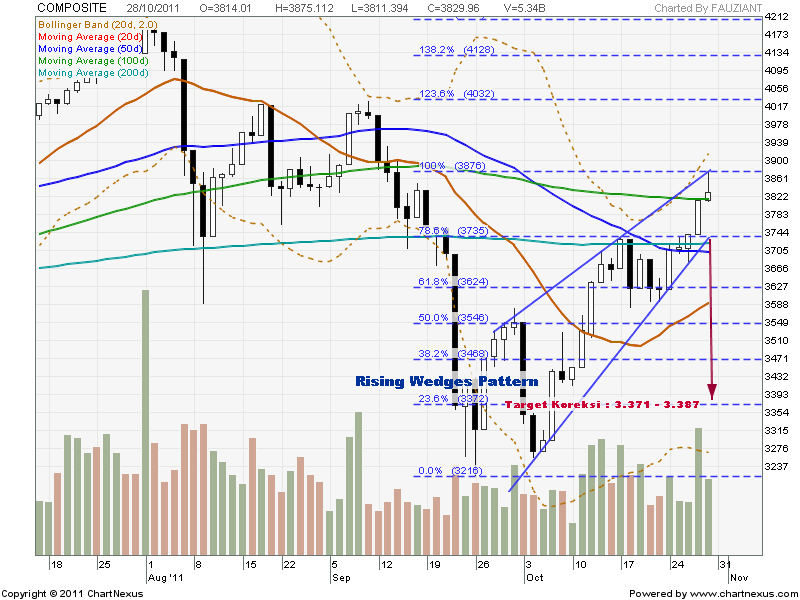

Monday, October 31, 2011

A Macro View Of The Week Ahead.

A Macro View Of The Week Ahead.

It’s only fitting that on Halloween we discuss a rather scary proposition. On Wednesday evening European leaders announced a “plan” details will come “later” to expand the aid to those in need.

It’s only fitting that on Halloween we discuss a rather scary proposition. On Wednesday evening European leaders announced a “plan” details will come “later” to expand the aid to those in need.

In lieu of physical capital which doesn’t seem to exist somehow these magicians will take nothing and turn it into something. Through the power of magic they will turn approximately 200 billion euros into 1 trillion.

So before you book tickets to Europe to experience this new found utopia perhaps it’s worth a look “under the hood” at some potential problems. In fact each potential problem actually builds upon one another creating a much more immediate risk. Did leaders in trying to solve one problem actually fast forward the pace of many more?

Debtors Have The Power

Imagine walking into your bank, telling the customer service agent that you can’t pay your loan but if they will cut it in half you should be fine. After the laughter subsides you are quickly asked to leave. In essence that is what Greece did. The debtor turned to the creditor and said you need to reduce our debt. You need to work with us.

The fear of Greece defaulting is a path the EU simply does not want to embark upon. European leaders made this very clear. They would rather forgive some debt on their terms versus facing a complete loss where they have no control. Ireland, Portugal, Spain and Italy paid close attention.

Size Of The EFSF

The EU was desperate to use the word trillion in their plan even if it is purely a function of leverage. Take roughly 200 billion Euros left in the EFSF fund, apply five fold leverage based on a 20% first loss guarantee and you get to where they “needed to be.” But if Greece debt had a default rate of 50% shouldn’t the leverage actually be two, not five?

In other words isn’t the fund really worth 400 billion Euros? A much smaller number that will do little if anything. Greece used up half of that on their own.

Moral Hazard

A phrase from 2008 is back. If I give my child $100 am I not “obligated” to give it to the other children? If the EU gives Greece 50% debt forgiveness why should they not do the same for Ireland and Portugal. What if Spain and Italy need help why should they not be treated similarly? I mean they are all part of the same union. It’s only “fair.”

Initially perhaps these countries will say Greece was a different circumstance and EU leaders are not allowing us to receive such favorable treatment. How long does that really last though when there are riots and protests in your streets demanding this wipe out of debt.

If a leader can either ask for billions in austerity from taxpayers or billions in debt forgiveness from bondholders what do you think is the easier path to follow?Why should an Irish taxpayer who contributed to the EFSF not be allowed to benefit as a Greek taxpayer does?

Bond Arbitrage

Italian and Spanish debt trades on the secondary market. With Greek debt suffering a 50% loss and no ability to hedge via CDS (credit default swaps) the prices of sovereign debt will trade well below par. Let’s assume Italian debt now trades for 70 cents on the dollar (for every $1 in par you only pay $.70). This new EFSF insured Italian debt will trade initially at par with a low coupon.

So in essence the new debt is really trading at 80 cents on the dollar because the fist 20 cents is guaranteed. Sounds good but why not buy on the secondary market at 70 cents? It’s the same underlying risk in terms of the Italian government.

So if buyers are gravitating to the cheaper, uninsured bonds won’t that force this new EFSF insured debt to either offer insurance above the 20% first loss, in this example 30%? They certainly won’t increase the coupon because the purpose of this plan is to reduce, not increase the debt service the Italian government must face. As stated above, the 20% or five fold leverage is comical at best and well under realistic levels.

Rating Risk

In September 2008 as the funding stress grew within the financial sector rating agencies began to “price in this risk” by downgrading various institutions. AIG for example faced with a downgrade found themselves in an immediate need to raise capital in an environment where they were shut out of the capital markets. The only way of preventing bankruptcy was for the government to inject capital. On September 12 AIG announced that in two weeks they would announce a reorganization plan to calm investors. Five days later they were bailed out by the Federal government.

Banks across the EU were told to raise over 100 billion Euro by June 2012. Many have argued that number is far below estimates. Already shut out of the capital markets these banks are selling assets to raise cash. All it takes now is a rating agency to downgrade them. AIG thought they had weeks. In reality they had days.

This may very well force the governments to assist them as the US assisted AIG. The problem here is France is at most risk of a downgrade themselves which would then put all of the pressure upon Germany to expand the EFSF.

Bottom Line

This fund does nothing. It has no capital so rather than buying debt it simply buys time. No sooner was the plan announced and Sarkozy and team were in China pleading for capital. Will China be the white knight? China already said their investment is contingent upon participation of others. Brazil already said they are not interested. Japan said they would contribute but they too are limited. How much can the IMF truly contribute?

The only source of real capital needed (which is really debt) is from taxpayers. Private investors are simply not willing to take on the risk. The only way to convince taxpayers is through a crisis. An event where the free world is once again portrayed to be at risk.

So in my view this plan did nothing but accelerate the timetable. Already there are rumblings from Ireland and Portugal. Moral hazard is alive and well and something the EU must now face as well. Now that is a truly scary proposition. (/www.elliottwavemarketservice.com)

In lieu of physical capital which doesn’t seem to exist somehow these magicians will take nothing and turn it into something. Through the power of magic they will turn approximately 200 billion euros into 1 trillion.

So before you book tickets to Europe to experience this new found utopia perhaps it’s worth a look “under the hood” at some potential problems. In fact each potential problem actually builds upon one another creating a much more immediate risk. Did leaders in trying to solve one problem actually fast forward the pace of many more?

Debtors Have The Power

Imagine walking into your bank, telling the customer service agent that you can’t pay your loan but if they will cut it in half you should be fine. After the laughter subsides you are quickly asked to leave. In essence that is what Greece did. The debtor turned to the creditor and said you need to reduce our debt. You need to work with us.

The fear of Greece defaulting is a path the EU simply does not want to embark upon. European leaders made this very clear. They would rather forgive some debt on their terms versus facing a complete loss where they have no control. Ireland, Portugal, Spain and Italy paid close attention.

Size Of The EFSF

The EU was desperate to use the word trillion in their plan even if it is purely a function of leverage. Take roughly 200 billion Euros left in the EFSF fund, apply five fold leverage based on a 20% first loss guarantee and you get to where they “needed to be.” But if Greece debt had a default rate of 50% shouldn’t the leverage actually be two, not five?

In other words isn’t the fund really worth 400 billion Euros? A much smaller number that will do little if anything. Greece used up half of that on their own.

Moral Hazard

A phrase from 2008 is back. If I give my child $100 am I not “obligated” to give it to the other children? If the EU gives Greece 50% debt forgiveness why should they not do the same for Ireland and Portugal. What if Spain and Italy need help why should they not be treated similarly? I mean they are all part of the same union. It’s only “fair.”

Initially perhaps these countries will say Greece was a different circumstance and EU leaders are not allowing us to receive such favorable treatment. How long does that really last though when there are riots and protests in your streets demanding this wipe out of debt.

If a leader can either ask for billions in austerity from taxpayers or billions in debt forgiveness from bondholders what do you think is the easier path to follow?Why should an Irish taxpayer who contributed to the EFSF not be allowed to benefit as a Greek taxpayer does?

Bond Arbitrage

Italian and Spanish debt trades on the secondary market. With Greek debt suffering a 50% loss and no ability to hedge via CDS (credit default swaps) the prices of sovereign debt will trade well below par. Let’s assume Italian debt now trades for 70 cents on the dollar (for every $1 in par you only pay $.70). This new EFSF insured Italian debt will trade initially at par with a low coupon.

So in essence the new debt is really trading at 80 cents on the dollar because the fist 20 cents is guaranteed. Sounds good but why not buy on the secondary market at 70 cents? It’s the same underlying risk in terms of the Italian government.

So if buyers are gravitating to the cheaper, uninsured bonds won’t that force this new EFSF insured debt to either offer insurance above the 20% first loss, in this example 30%? They certainly won’t increase the coupon because the purpose of this plan is to reduce, not increase the debt service the Italian government must face. As stated above, the 20% or five fold leverage is comical at best and well under realistic levels.

Rating Risk

In September 2008 as the funding stress grew within the financial sector rating agencies began to “price in this risk” by downgrading various institutions. AIG for example faced with a downgrade found themselves in an immediate need to raise capital in an environment where they were shut out of the capital markets. The only way of preventing bankruptcy was for the government to inject capital. On September 12 AIG announced that in two weeks they would announce a reorganization plan to calm investors. Five days later they were bailed out by the Federal government.

Banks across the EU were told to raise over 100 billion Euro by June 2012. Many have argued that number is far below estimates. Already shut out of the capital markets these banks are selling assets to raise cash. All it takes now is a rating agency to downgrade them. AIG thought they had weeks. In reality they had days.

This may very well force the governments to assist them as the US assisted AIG. The problem here is France is at most risk of a downgrade themselves which would then put all of the pressure upon Germany to expand the EFSF.

Bottom Line

This fund does nothing. It has no capital so rather than buying debt it simply buys time. No sooner was the plan announced and Sarkozy and team were in China pleading for capital. Will China be the white knight? China already said their investment is contingent upon participation of others. Brazil already said they are not interested. Japan said they would contribute but they too are limited. How much can the IMF truly contribute?

The only source of real capital needed (which is really debt) is from taxpayers. Private investors are simply not willing to take on the risk. The only way to convince taxpayers is through a crisis. An event where the free world is once again portrayed to be at risk.

So in my view this plan did nothing but accelerate the timetable. Already there are rumblings from Ireland and Portugal. Moral hazard is alive and well and something the EU must now face as well. Now that is a truly scary proposition. (/www.elliottwavemarketservice.com)

Thursday, October 20, 2011

Tuesday, October 18, 2011

Friday, October 7, 2011

Tuesday, June 21, 2011

Friday, May 20, 2011

Pemerintah AS Terancam Gagal Bayar

Ketidakmampuan membayar utang jatuh tempo tidak hanya akan menambah ongkos pinjaman pemerintah, tapi juga pinjaman swasta.

Ketidakmampuan membayar utang jatuh tempo tidak hanya akan menambah ongkos pinjaman pemerintah, tapi juga pinjaman swasta.MENTERI Keuangan Amerika Serikat (AS) Timothy Geithner menyatakan kondisi utang pemerintahnya hampir menyentuh batas tertingginya, yakni US$14,3 triliun. Ia memperingatkan kondisi itu bisa berakibat bencana dan resesi baru jika Washington tidak bisa mengadakan utang baru.

Gagalnya Kongres AS menaikkan batas utang hingga hari ini memaksa Geithner merealokasi anggaran untuk memenuhi kewajibannya, termasuk membayar para pemegang obligasi mereka.

Namun, tindakan tersebut hanya bisa dilakukan hingga 2 Agustus. Setelah itu, Washington akan terpaksa mengemplang pembayaran yang dapat mengguncang paiar keuangan dunia.

"Default dapat memicu bencana tidak terkira terhadap ekonomi kita, mengurangi pertumbuhan secara signifikan,dan meningkatkan pengangguran," ujar Geithner dalam suratnya tertanggal Jumat (13/5) kepada senator asal Partai Demokrat Michael Ben-net seperti dikutip kantor berita Renters, kemarin.Pemerintahan Obama dan para pembuat kebijakan hingga kini masih terus berseberangan mengenai cara mengekang laju utang AS. Partai Republik berkukuh menolak penaikan batas utang tanpa adanya pemotongan anggaran belanja secara lebih mendalam.

Namun, Geithner mengingatkan default, atau gagal bayar, tidak hanya akan menambah ongkos pinjaman bagi pemerintah, tapi juga bagi rata-rata rakyat AS, kalangan bisnis, dan pemerintah lokal.

"Kenaikan bunga obligasi akan meningkatkan ongkos sebuah keluarga dalam membeli rumah, kendaraan, atau untuk menyekolahkan anak mereka ke perguruan tinggi. Hal ini juga akan menyulitkan pengusaha memperoleh pinjaman untuk memulai usahaatau berinvestasi," ujarnya.

Hingga kini, negara ekonomi terbesar dunia tersebut masih dalam tahap pemulihan dari krisis finansial 2007-2009. Akan tetapi, 13,7 juta orang telah kehilangan pekerjaan dan tingginya harga bahan bakar minyak (BBM) serta pangan mengancam proses pemulihan ekonomi. "Kontraksi tiba-tiba (belanja pemerintah) mungkin akan mendorong kita ke resesi double-dip," kata Geithner.

Saat ini Washington diperkirakan mencetak utang US$125 miliar per bulan. Sampai Kamis (12/5), batas pinjaman yang tersisa hanya US$38 miliar. Geithner dan Gubernur Federal Reserve Ben Bernanke berulang kali mendesak agar Kongres AS segera menyetujui penambahan batas utang.

Ancaman inflasi

Pada kesempatan lain Washington mencatat inflasi April merupakan tertinggi dalam 2,5 tahun. Harga bahan bakar dan pangan menjadi kontributor utama. Namun, pertan-da adanya kenaikan harga konsumen masih sangat kecil untuk dapat menyulitkan The Fed.Di sisi lain, sebuah survei memperlihatkan kenaikan tingkat inflasi juga menimbulkan kecemasan masyarakat AS mengenai kondisi keuangan mereka.

Harga konsumen tercatat meningkat 0,4% pada April, melambat ketimbang 0,5, pada Maret. Jumat (13/5) lalu, Departemen Tenaga Kerja mencatat kenaikan tersebut mendongkrak inflasi menyentuh angka 3,2% dan tercatat sebagai kenaikan inflasi tahunan tertinggi sejak Oktober 2008.

Terlepas dari gejolak harga pangan dan ongkos energi, inflasi inti naik tipis 0,2% dari Maret lalu. Kenaikan 1,3. dalam 12 bulan merupakan kenaikan tertinggi sejak Februari 2010.

The Fed bahkan memperkirakan angka tersebut akan mendekati 2% dalam beberapa waktu ke depan.

Thursday, May 19, 2011

Wednesday, May 18, 2011

Tuesday, May 10, 2011

Kuasi Reorganisasi

I Made B. Tirthayatra

Warta Bapepam-LK

Perusahaan-perusahaan yang laporan keuangannya berisi saldo laba negatif, atau dikenal dengan istilah defisit, mengalami beberapa hambatan dibanding perusahaan yang tidak mengalami defisit. Hambatan-hambatan tersebut antara lain adalah relatif lebih sulitnya memperoleh pendanaan dibanding dengan perusahaan yang tidak mengalami defisit. Kreditor biasanya memberikan persyaratan pinjaman yang lebih tinggi kepada perusahan yang defisit dibanding kepada perusahaan yang memiliki saldo laba positif. Disamping itu, investor juga mengalami kerugian karena perusahaan yang defisit tidak diperkenankan oleh Undang-Undang tentang Perseroan terbatas untuk membagi deviden.

Perusahaan-perusahaan yang laporan keuangannya berisi saldo laba negatif, atau dikenal dengan istilah defisit, mengalami beberapa hambatan dibanding perusahaan yang tidak mengalami defisit. Hambatan-hambatan tersebut antara lain adalah relatif lebih sulitnya memperoleh pendanaan dibanding dengan perusahaan yang tidak mengalami defisit. Kreditor biasanya memberikan persyaratan pinjaman yang lebih tinggi kepada perusahan yang defisit dibanding kepada perusahaan yang memiliki saldo laba positif. Disamping itu, investor juga mengalami kerugian karena perusahaan yang defisit tidak diperkenankan oleh Undang-Undang tentang Perseroan terbatas untuk membagi deviden.

Adanya hambatan-hambatan tersebut menimbulkan kebutuhan bagi perusahaan-perusahaan yang mengalami defisit untuk menghapus saldo defisit dari laporan keuangan mereka. Sebenarnya saldo defisit akan terhapus apabila akumulasi laba bersih pada tahun-tahun berikutnya cukup besar untuk menutup defisit. Namun apabila saldo defisit sudah sangat besar, maka akan memakan waktu sangat lama bagi perusahaan untuk menutup defisitnya jika hanya mengandalkan laba bersih perusahaan. Satu cara yang memungkinkan perusahaan mengeliminasi defisit tanpa semata-mata menggunakan laba bersih adalah dengan melakukan kuasi-reorganisasi.

Pernyataan Standar Akuntansi Keuangan No. 51 (Revisi 2003) tentang Akuntansi Kuasi-Reorganisasi mendefinisikan kuasi-reorganisasi sebagai reorganisasi, tanpa melalui reorganisasi nyata, yang dilakukan dengan menilai kembali akun-akun aktiva dan kewajiban pada nilai wajar dan mengeliminasi saldo laba negatif atau defisit. Adanya keterangan tanpa melalui reorganisasi nyata pada definisi kuasi-reorganisasi adalah karena pada kuasi reorganisasi tidak terdapat restrukturisasi nyata seperti restrukturisasi hutang atau adanya arus dana secara nyata. Pada kuasi-reorganisasi yang ada hanyalah penilaian kembali seluruh aktiva dan kewajiban pada nilai wajarnya dan penghapusan defisit ke beberapa akun ekuitas.

Beberapa emiten yang melakukan kuasi reorganisasi sejak tahun 2003 sampai dengan tahun 2007 adalah sebagai berikut:

Tabel 1

Daftar Emiten yang melakukan kuasi-reorganisasi

tahun 2003 sampai dengan 2007

Ketentuan yang wajib dipenuhi oleh perusahaan dalam melaksanakan kuasi-reorganisasi adalah PSAK No. 51 tentang Akuntansi Kuasi-Reorganisasi, Undang-Undang tentang Perseroan Terbatas, dan Anggaran Dasar Perusahaan yang bersangkutan. Khusus bagi Emiten dan Perusahaan Publik, disamping ketentuan di atas juga wajib mengikuti Peraturan Bapepam-LK No. IX.L.1 tentang Tata Cara Pelaksanaan Kuasi Reorganisasi. Peraturan ini mewajibkan adanya keterbukaan informasi yang memadai bagi pemegang saham dan mewajibkan perusahaan untuk memperoleh persetujuan RUPS. Dengan Peraturan tersebut diharapkan bahwa pelaksanaan kuasi-reorganisasi oleh Emiten dan Perusahaan Publik semakin memiliki landasan hukum yang jelas dan kepentingan pemegang saham masyarakat semakin terlindungi. Disamping itu, sehubungan dengan pelaksanaan RUPS Emiten dan Perusahaan Publik wajib mengikuti Peraturan Bapepam-LK No. X.I.1 tentang Rencana dan Pelaksanaan Rapat Umum Pemegang Saham.

Peraturan-peraturan di atas mencakup berbagai aspek yang terkait dengan pelaksanaan kuasi-reorganisasi oleh perusahaan pada umumnya, dan Emiten dan Perusahaan Publik pada khususnya, seperti aspek keterbukaan informasi, perlindungan pemegang saham, perlakuan akuntansi, dsb. Berdasarkan peraturan-peraturan di atas, berikut adalah intisari atas hal-hal yang perlu diperhatikan dalam melaksanakan kuasi-reorganisasi oleh Emiten dan Perusahaan Publik.

Kondisi yang harus dipenuhi oleh Emiten dalam melakukan kuasi reorganisasi

Kewajiban untuk mengalami saldo laba negatif selama 3 tahun berturut-turut dalam jumlah yang material, dan memiliki prospek yang baik dimaksudkan agar tidak setiap Emiten dan Perusahaan Publik yang mengalami defisit dapat melakukan kuasi reorganisasi. Sebagaimana disebutkan di atas bahwa kuasi-reorganisasi bukan merupakan reorganisasi yang nyata, sehingga kesempatan untuk melakukan kuasi-reorganisasi ini hanya diberikan kepada perusahaan yang benar-benar membutuhkannya. Dengan persyaratan ketat sebagaimana disebutkan dalam PSAK No. 51 dan Peraturan No. IX.L.1 maka hanya Emiten dan Perusahaan Publik yang defisitnya bernilai material dan telah berlangsung cukup lama, dan memiliki prospek yang baiklah yang dapat melakukan kuasi reorganisasi.

Adapun kewajiban bahwa saldo laba setelah proses kuasi-reorganisasi harus nol memiliki dua tujuan. Pertama kuasi-reorganisasi tidak boleh dilakukan jika tujuannya hanya sekedar mengurangi defisit, namun harus benar-benar untuk menghapus defisit. Apabila setelah dilakukan penilaian kembali aktiva dan kewajiban ternyata nilainya tidak cukup untuk menghapus seluruh defisit maka Emiten dan Perusahaan Publik publik tidak boleh melakukan kuasi-reorganisasi. Tujuan lainnya adalah agar kuasi reorganisasi tidak digunakan untuk meningkatkan saldo laba positif. Apabila Kuasi Reorganisasi dapat digunakan untuk menambah saldo laba positif maka tujuan semula untuk membantu perusahaan yang terbebani defisit dapat disalahgunakan untuk meningkatkan saldo laba tersebut.

Kewajiban untuk memperoleh persetujuan Rapat Umum Pemegang Saham merupakan salah satu bentuk perlindungan terhadap pemegang saham. Hal ini karena melalui RUPS pemegang saham memiliki kesempatan untuk mencegah rencana kuasi-reorganisasi apabila rencana tersebut dipandang merugikan kepentingan pemegang saham. Disamping itu, Perlindungan tersebut didapat pemegang saham dalam bentuk adanya keterbukaan informasi terkait dengan rencana kuasi-reorganisasi sehingga pemegang saham dapat menentukan keputusan dengan tepat dalam RUPS.

Berdasarkan PSAK No. 51 dan Peraturan Bapepam-LK Nomor IX.L.1, Emiten dan Perusahaan Publik hanya dapat melakukan Kuasi Reorganisasi apabila memenuhi seluruh persyaratan dan kondisi yang ditetapkan. Persyaratan dan kondisi tersebut adalah perusahaan mengalami saldo laba negatif selama 3 (tiga) tahun berturut-turut dalam jumlah yang material, memiliki status kelancaran usaha dan memiliki prospek yang baik pada saat kuasi-reorganisasi dilakukan, saldo laba setelah proses kuasi-reorganisasi harus nol, memperoleh persetujuan Rapat Umum Pemegang Saham, dan pelaksanaan kuasi-reorganisasi tidak bertentangan dengan peraturan perundangan yang berlaku.

Kewajiban untuk mengalami saldo laba negatif selama 3 tahun berturut-turut dalam jumlah yang material, dan memiliki prospek yang baik dimaksudkan agar tidak setiap Emiten dan Perusahaan Publik yang mengalami defisit dapat melakukan kuasi reorganisasi. Sebagaimana disebutkan di atas bahwa kuasi-reorganisasi bukan merupakan reorganisasi yang nyata, sehingga kesempatan untuk melakukan kuasi-reorganisasi ini hanya diberikan kepada perusahaan yang benar-benar membutuhkannya. Dengan persyaratan ketat sebagaimana disebutkan dalam PSAK No. 51 dan Peraturan No. IX.L.1 maka hanya Emiten dan Perusahaan Publik yang defisitnya bernilai material dan telah berlangsung cukup lama, dan memiliki prospek yang baiklah yang dapat melakukan kuasi reorganisasi.

Adapun kewajiban bahwa saldo laba setelah proses kuasi-reorganisasi harus nol memiliki dua tujuan. Pertama kuasi-reorganisasi tidak boleh dilakukan jika tujuannya hanya sekedar mengurangi defisit, namun harus benar-benar untuk menghapus defisit. Apabila setelah dilakukan penilaian kembali aktiva dan kewajiban ternyata nilainya tidak cukup untuk menghapus seluruh defisit maka Emiten dan Perusahaan Publik publik tidak boleh melakukan kuasi-reorganisasi. Tujuan lainnya adalah agar kuasi reorganisasi tidak digunakan untuk meningkatkan saldo laba positif. Apabila Kuasi Reorganisasi dapat digunakan untuk menambah saldo laba positif maka tujuan semula untuk membantu perusahaan yang terbebani defisit dapat disalahgunakan untuk meningkatkan saldo laba tersebut.

Kewajiban untuk memperoleh persetujuan Rapat Umum Pemegang Saham merupakan salah satu bentuk perlindungan terhadap pemegang saham. Hal ini karena melalui RUPS pemegang saham memiliki kesempatan untuk mencegah rencana kuasi-reorganisasi apabila rencana tersebut dipandang merugikan kepentingan pemegang saham. Disamping itu, Perlindungan tersebut didapat pemegang saham dalam bentuk adanya keterbukaan informasi terkait dengan rencana kuasi-reorganisasi sehingga pemegang saham dapat menentukan keputusan dengan tepat dalam RUPS.

Penilaian Aktiva dan Kewajiban

Apabila seluruh kondisi yang dipersyaratkan tersebut diperkirakan dapat terpenuhi, langkah pertama yang dilakukan adalah melakukan penilaian kembali seluruh aktiva dan kewajiban perusahaan pada nilai wajarnya. Karena merupakan prasyarat dalam melakukan kuasi-reorganisasi, maka penilaian kembali ini tetap wajib dilakukan meskipun saldo akun-akun ekuitas yang ada sebelum dilakukannya penilaian kembali telah cukup untuk menutup defisit yang ada. Penilaian kembali bahkan tetap harus dilakukan meskipun penilaian tersebut menghasilkan nilai aset bersih yang lebih rendah dibanding nilai sebelum penilaian kembali. Peraturan Bapepam-LK nomor IX.L.1 menyatakan bahwa penilaian kembali aktiva tetap harus dilakukan oleh Penilai yang terdaftar di Bapepam-LK, dan penilaian kembali kewajiban dan aktiva selain aktiva tetap dilakukan oleh Pihak independen.

Sehubungan dengan penilaian aktiva tetap, terdapat ketentuan perpajakan yang perlu diperhatikan. Dalam hal penilaian kembali tersebut dimintakan persetujuan dari Direktorat Jenderal Pajak, maka atas selisih lebih penilaian kembali tersebut akan terkena pajak. Hal ini karena peningkatan nilai aktiva tersebut pada gilirannya akan meningkatkan biaya penyusutan sehingga akan mengurangi pajak yang harus dibayar oleh perusahaan.

Sebaliknya, apabila penilaian kembali tersebut tidak dimintakan persetujuan Direktorat Jenderal Pajak maka atas peningkatan nilai aktiva tetap tersebut tidak dikenakan pajak. Hal ini karena Direktorat Jenderal Pajak tetap mengakui nilai aktiva tetap perusahaan sebesar nilai sebelum penilaian kembali dan akan menghitung biaya penyusutan atas aktiva tetap berdasarkan nilai sebelum penilaian kembali tersebut. Perbedaan antara nilai aktiva tetap yang tercatat pada laporan keuangan dengan yang diakui oleh Direktorat Jenderal Pajak ini menjadi perbedaan temporer yang akan direkonsiliasi pada saat perhitungan pajak perusahaan.

Eliminasi Defisit

Tabel 2

Neraca PT ABC sebelum dan setelah penilaian kembali seluruh aktiva dan kewajiban

Setelah perusahaan mengetahui nilai wajar dari seluruh aktiva dan kewajibannya, maka perusahaan dapat memperkirakan apakah selisih penilaian kembali aktiva dan kewajibannya cukup besar untuk menutup saldo negatif. PSAK No. 51 mengatur akun-akun mana saja yang digunakan untuk menutup saldo defisit, serta mengatur urutan prioritas dari akun-akun tersebut. Urutan pertama adalah Cadangan Umum. Kedua, cadangan khusus. Ketiga, selisih penilaian aktiva dan kewajiban dan selisih penilaian sejenisnya (misalnya selisih penilaian efek tersedia untuk dijual, selisih transaksi perubahan ekuitas anak perusahaan/perusahaan asosiasi, dan pendapatan komprehensif). Keempat, tambahan modal disetor dan sejenisnya (misalnya selisih kurs setoran modal). Kelima, yang terakhir, adalah modal saham. Penggunaan modal saham untuk menutup defisit dilakukan dengan cara menurunkan nilai nominal saham, dan menggunakan selisih antara nilai nominal lama dengan nilai nominal yang baru untuk menutup sisa defisit yang belum terhapus oleh akun-akun ekuitas lainnya. Apabila setelah semua saldo akun-akun tersebut habis digunakan namun ternyata defisit Emiten dan Perusahaan Publik belum sepenuhnya terhapus, maka kuasi reorganisasi tidak dapat dilakukan.

Sebagai ilustrasi, suatu perusahaan yang bernama PT ABC, memiliki total aktiva Rp. 500 milyar, total kewajiban Rp. 300 milyar dan total ekuitas Rp. 200 milyar, dimana saldo ekuitas tersebut terdiri dari Defisit Rp. 100 milyar, Cadangan Umum Rp. 25 milyar, Cadangan Khusus Rp. 25 milyar, Modal Disetor sebesar Rp. 250 milyar. Perusahaan tersebut bermaksud untuk menghapus defisitnya melalui kuasi-reorganisasi, dan mulai melakukan penilaian kembali aktiva dan kewajibannya. Setelah dilakukan penilaian kembali, nilai total aktiva menjadi Rp. 600 milyar, dan nilai kewajiban tidak berubah, sehingga terdapat saldo selisih penilaian aktiva dan kewajiban menjadi Rp. 100 milyar. Tabel 2 menggambarkan perbandingan neraca PT ABC sebelum dan setelah penilaian kembali aktiva dan kewajiban:

Tabel 2

Neraca PT ABC sebelum dan setelah penilaian kembali seluruh aktiva dan kewajiban

Setelah dilakukan penilaian kembali aktiva dan kewajiban maka perusahaan mulai menutup defisit dengan akun-akun ekuitas berdasarkan urutan sebagaimana ditentukan oleh PSAK No. 51 di atas. Berdasarkan posisi akun-akun ekuitas yang dimiliki perusahaan, maka saldo yang digunakan untuk menutup defisit Rp. 100 milyar adalah saldo cadangan khusus seluruhnya, saldo cadangan umum seluruhnya, dan saldo selisih penilaian kembali aktiva dan kewajiban sebesar Rp. 50 milyar. Setelah defisit mencapai angka nol, maka saldo cadangan khusus dan cadangan umum menjadi nol, saldo selisih penilaian kembali aktiva dan kewajiban tersisa sebesar Rp. 50 milyar.

Tabel 3 menggambarkan posisi ekuitas PT ABC sebelum dan setelah kuasi reorganisasi dilaksanakan.

Tabel 3

Ekuitas PT ABC sebelum dan setelah eliminasi defisit

Ekuitas PT ABC sebelum dan setelah eliminasi defisit

Keterbukaan Informasi dan Rapat Umum Pemegang Saham

Berdasarkan perhitungan yang dilakukan, apabila perusahaan memandang kuasi-reorganisasi dapat dilaksanakan maka langkah selanjutnya adalah mendapatkan persetujuan RUPS. Peraturan Nomor IX.L.1 menyatakan bahwa kuasi-reorganisasi hanya dapat dilaksanakan setelah mendapat persetujuan Rapat Umum Pemegang Saham. Dengan adanya kewajiban ini maka pemegang saham yang tidak setuju dengan rencana kuasi-reorganisasi memiliki kesempatan untuk mencegah pelaksanaan rencana kuasi-reorganisasi. Apabila mayoritas pemegang saham tidak menyetujui rencana kuasi-reorganisasi maka kuasi-reorganisasi tidak dapat dilaksanakan.

Dalam rangka mendapat persetujuan RUPS ini maka Emiten dan Perusahaan Publik wajib menyampaikan keterbukaan informasi kepada pemegang saham sehingga keputusan pemegang saham pada saat RUPS akan diambil berdasarkan informasi yang memadai. Untuk itu maka Emiten dan Perusahaan Publik wajib menyiapkan secara cermat aspek keterbukaan sebagaimana ditetapkan dalam Peraturan Bapepam-LK Nomor IX.L.1. Hal-hal yang wajib disampaikan tersebut antara lain adalah rencana, tujuan dan alasan dilakukannya kuasi reorganisasi, jadwal pelaksanaan kuasi reorganisasi, ikhtisar data keuangan penting selama 3 (tiga) tahun terakhir, status kelangsungan usaha, hasil penilaian nilai wajar aktiva dan kewajiban, neraca sebelum kuasi reorganisasi yang diaudit dan proforma neraca sesudah kuasi reorganisasi, termasuk rincian perhitungan eliminasi saldo laba negatif, yang direview, dan pendapat dari Akuntan mengenai kesesuaian penerapan prosedur dan ketentuan dalam pelaksanaan kuasi reorganisasi dengan prinsip akuntansi yang berlaku umum, termasuk penyesuaian-penyesuaian akuntansi yang ada.

Berdasarkan Peraturan Bapepam-LK No. IX.I.1 tentang Rencana dan Pelaksanaan RUPS, maka keterbukaan informasi kepada pemegang saham sebagaimana disebutkan di atas wajib disampaikan kepada Bapepam-LK selambat-lambatnya 7 (tujuh) hari sebelum pengumuman RUPS. Adapun jadwal pengumuman RUPS, termasuk penyampaian keterbukaan informasi mengenai kuasi-reorganisasi kepada publik, dilaksanakan sesuai jadwal yang ditetapkan dalam Anggaran Dasar Emiten dan Perusahaan Publik. Dengan disampaikannya keterbukaan informasi kepada publik diharapkan pemegang saham akan mendapat informasi yang memadai untuk mengambil keputusan dalam RUPS.

Pengungkapan dalam laporan keuangan setelah pelaksanaan kuasi-reorganisasi

Setelah pelaksanaan kuasi-reorganisasi, informasi tentang kuasi-reorganisasi wajib dimuat dalam laporan keuangan Emiten dan Perusahaan Publik sesuai dengan PSAK No. 51 tentang Akuntansi Kuasi-Reorganisasi. PSAK ini berusaha memastikan agar informasi mengenai kuasi-reorganisasi benar-benar sampai kepada pembaca laporan keuangan.

Mengingat bahwa kuasi-reorganisasi bukan merupakan reorganisasi nyata, maka disamping persyaratannya harus sangat ketat, juga harus terdapat jaminan bahwa informasi mengenai kuasi-reorganisasi ini terbaca oleh pembaca laporan keuangan. Untuk itu menjamin hal tersebut maka PSAK No. 51 mewajibkan laporan keuangan tahunan untuk menyajikan neraca akhir periode sebelum kuasi-reorganisasi, neraca per tanggal kuasi reorganisasi dan neraca akhir periode terakhir. Dengan munculnya informasi mengenai kuasi-reorganisasi secara signifikan di neraca, diharapkan informasi tersebut tidak akan terlewat oleh pembaca laporan keuangan.

Disamping penyajian di neraca, PSAK No. 51 juga mewajibkan adanya pengungkapan dalam catatan atas laporan keuangan mengenai alasan melakukan kuasi-reorganisasi, status going concern perusahaan dan rencana manajemen dan pemegang saham setelah kuasi reorganisasi yang menggambarkan prospek usaha di masa depan, jumlah saldo laba negatif yang dieliminasi dalam neraca dan jumlah tersebut disajikan selama tiga tahun berturut-turut sejak kuasi-reorganisasi, metode penentuan nilai wajar yang digunakan untuk menilai aset dan kewajiban pada saat dilakukan kuasi-reorganisasi, rincian dari jumlah yang membentuk akun selisih peniliaan aset dan kewajiban sebelum digunakan untuk mengeliminasi defisit, dan keterangan tanggal terjadinya kuasi reorganisasi pada akun saldo laba dalam neraca untuk jangka waktu 10 tahun ke depan sejak kuasi reorganisasi. Dengan diungkapkannya keterangan mengenai kuasi-reorganisasi dalam laporan keuangan sampai dengan 10 tahun sejak pelaksanaannya, maka informasi tersebut tidak dengan mudah dilupakan oleh para pemangku kepentingan perusahaan tersebut.

Demikianlah beberapa peraturan yang harus diperhatikan oleh Emiten dan Perusahaan Publik dalam melakukan kuasi-reorganisasi. Sebagaimana pada peraturan Bapepam-LK lainnya, peraturan-peraturan tersebut bertujuan untuk memberikan landasan hukum yang jelas bagi pelaksanaan kuasi reorganisasi, dan memberikan perlindungan terhadap kepentingan pemegang saham melalui keterbukaan informasi dan adanya hak untuk mencegah kuasi-reorganisasi jika pemegang saham memandang kuasi-reorganisasi merugikan kepentingannya. (Made)

Monday, May 9, 2011

Trading Wisdom

•Buy low, sell high.

•Buy high, sell higher.

•Don’t fight the Fed.

•Don’t fight the tape.

•Pigs get fat, hogs get slaughtered. Or: Pigs get FED, hogs get slaughtered.

•Bulls make money. Bears make money. Pigs get slaughtered.

•Trade in the direction of the trend.

•The trend is your friend.

•The trend is not your friend when it ends.

•The crowd is right during the trends but wrong at both ends. (Humphrey B. Neill)

•Buy the dips, sell the rallies.

•Buy the rumor, sell the fact.

•Buy into bad news and sell into good news.

•Buy the panic, sell the greed.

•Buy strength, sell weakness.

•Never short a dull market.

•Cut losses short, let profits run.

•When in doubt, stay out.

•It’s easier to stay out than to get out.

•Get out when you can, not when you have to.

•Minimize losses.

•Never let a winner turn into a loser.

•Never let a small loss turn into a big loss.

•Lose your opinion, not your money.

•Trade what you see, not what you think.

•When in doubt, sell. You will usually get another chance in something else.

•Quickly exit losing trades and move on to the next opportunity.

•Date them, don’t marry them.

•You can’t go broke taking profits.

•A profitable trade is a good trade.

•Take profits relentlessly.

•Profits aren’t as important as preserving your capital.

•Manage the risk and the profits will take care of themselves.

•It’s better to own too few shares than too many.

•Average up, not down. Add to winners, not losers.

•There are more fools among buyers than among sellers.

•The open belongs to the amateurs and the close belongs to the professionals.

•Plan your trades. Trade your plan.

•Always sell what shows you a loss and keep what shows you a profit. (Reminiscences of a Stock Operator)

•There are few if any chronic bears, as pessimists have a hard time making a living in America. (John Rothchild)

•There’s nothing wrong with cash. It gives you time to think. (Robert Pretcher, Jr.)

•Predetermine the exit strategy for all trades. Always have a plan for selling, as well as for buying.

•Know the fundamentals. Trade the technicals.

•Volume precedes price.

•Price has memory.

•Bottoms take longer to form than tops.

•Buy at support, sell at resistance.

•Sell on the stall before the fall.

•Buy ‘em when they’re sleepin’, hold ‘em when they’re creepin’, sell ‘em when they’re leapin’.

•The best time to buy is when blood is running in the streets. (Nathan M. Rothschild)

•Buy when most people are selling, and sell when most people are buying.

•Buy from the scared, sell to the greedy.

•Buy their pain, not their gain.

•Beat the crowd in and out the door. You have to take their money before they take yours, period.

•Successful traders are quick to change their minds and have little pride of opinion. (Don Worden)

•The most profitable traders spend 80 percent of their time finding a fast-moving market, and 20 percent of their time trading it. (David Bowden)

•There’s only one indicator that counts: The Check-Book Indicator. (David Bowden)

•Risk varies inversely with knowledge. (Irving Fisher)

•I made my money because I always got out too soon. (Bernard Baruch)

•Don’t try to buy at the bottom and sell at the top. It can’t be done except by liars. (Bernard Baruch)

•Even being right three or four times out of 10 should yield a person a fortune if they have the sense to cut losses quickly. (Bernard Baruch)

•Throughout all my years of investing I’ve found that the big money was never made in the buying or the selling. The big money was made in the waiting. (Jesse Livermore)

•The faster a stock has climbed, the quicker it will fall. (Menschel)

•The easier information arrives, the less valuable it is. (Menschel)

•The more certain the crowd is, the surer it is to be wrong. (Menschel)

•It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong. (George Soros)

•My approach works not by making valid predictions but by allowing me to correct false ones. (George Soros)

--------------------------------------------------------------------------------

Warren Buffet

•Occasionally, successful investing requires inactivity.

•In this game, the market has to keep pitching, but you don’t have to swing. You can stand there with the bat on your shoulder until you get a fat pitch.

•I will tell you the secret of getting rich on Wall Street. You try to be greedy when others are fearful, and you try to be very fearful when others are greedy.

•I’d be a bum on the street with a tin cup if the markets were always efficient.

•I don’t try to jump over 7-foot bars, I look around for 1-foot bars that I can step over.

•For investors as a whole, returns decrease as motion increases.

•The market, like the Lord, helps those who help themselves. But unlike the Lord, the market does not forgive those who know not what they do.

•Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it.

•Risk comes from not knowing what you’re doing.

•It’s only when the tide goes out that you know who’s been swimming naked.

--------------------------------------------------------------------------------

•Buy at the point of maximum pessimism and sell at the point of maximum optimism. (Sir John Templeton, founder of Templeton Funds)

•Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria. (Sir John Templeton)

•We’re all just one trade away from humility. (WallStreet, the movie)

•As the notorious stock manipulator Daniel Drew allegedly said, “To speckilate as an outsider is like trying to drive black pigs in the dark.”

•If you don’t like the odds, don’t bet. (Jesse Livermore)

•Price is king, but volume is the power behind the price. (Don Warden)

•The market can remain irrational longer than you can remain solvent. (Keynes)

•Bear markets begin in good times. Bull markets begin in bad times.

•Never confuse genius with a bull market.

•Just because the price goes up doesn’t mean you’re right; just because the price goes down doesn’t mean you’re wrong. (Peter Lynch)

•Money goes where it is wanted and stays where it is well treated. (Walter Wriston)

•Rallies in bear markets die on low volume. (Art Cashin on CNBC)

•Volume is validity. If enough people believe in something, it moves. (Art Cashin on CNBC)

•Trading isn’t a game of luck. It’s a game of probability.

•Prosperity ends in a crisis. The error of optimism dies in the crisis, but in dying it gives birth to an error of pessimism. This new error is born, not an infant, but a giant. (Arthur Cecil Pigou)

•Capitalism without failure is like religion without sin. (Economist and Carnegie Mellon professor Allan Meltzer)

•Money: Power at its most liquid. -Mason Cooley

•The bigger the top, the bigger the drop.

Tuesday, May 3, 2011

Monday, May 2, 2011

Thursday, April 28, 2011

CPIN

Give me 5

Beta : 1.46

Market Cap (Mil.) : Rp. 31,696,020.00

Shares Outstanding (Mil.) : 16,422.81

Annual Dividend : 39.20

Yield (%) : 2.03

P/E (TTM) : 14.34

EPS (TTM) : 37.09

ROI : 51.96

ROE : 59.81

Market Cap (Mil.) : Rp. 31,696,020.00

Shares Outstanding (Mil.) : 16,422.81

Annual Dividend : 39.20

Yield (%) : 2.03

P/E (TTM) : 14.34

EPS (TTM) : 37.09

ROI : 51.96

ROE : 59.81

Wednesday, April 27, 2011

JSX vs Sektoral

JSX vs Agri

JSX vs Basic Industry

JSX vs Consumer

JSX vs Finance

JSX vs Infrastructure

JSX vs Manufacture

JSX vs Mining

JSX vs Misc Industry

JSX vs Property

JSX vs Trade

Tuesday, April 26, 2011

MEDC

Wave pattern "Zigzag" ; CS : Last Engulfing Bottom ; Falling Wedges

Support : 2.700 ; R1 : 2.800 ; R2 : 2.900

Support : 2.700 ; R1 : 2.800 ; R2 : 2.900

Beta : 1.05

Market Cap (Mil.) : Rp. 9,330,864.00

Shares Outstanding (Mil.) : 3,332.45

Annual Dividend : 25.96

Yield (%) : 0.93

P/E (TTM) : 11.45

EPS (TTM) : 331.80

ROI : 5.41

ROE : 11.11

Monday, April 25, 2011

UNTR

Symmetrical Triangles Wave Pattern (3-3-3-3-3)

Bull Continuation wait for the sub wave E

Beta : 1.31

Market Cap (Mil.) : Rp. 76,646,472.00

Shares Outstanding (Mil.) : 3,326.88

Annual Dividend : 490.00

Yield (%) : 2.12

Financials

P/E (TTM) : 19.84

EPS (TTM) : 1.45

ROI : 21.04

ROE : 25.84

Tuesday, April 19, 2011

USD Index

USD Index

Pattern : Falling Wedges

Breakup : 75.22 TP : 78.8

"USD naik, Harga commodity turun ?"

Update 24 April 2011

breakdown tren channel lower menuju sub wave 9 of "unknown wave extension" ?

Wall Street shares slump as S&P downgrades US debt outlook

Ratings agency cuts long-term outlook from stable to negative for first time since Pearl Harbor attack 70 years ago

Shares fell heavily on Wall Street on Monday after a leading ratings agency fanned fears of Europe's debt crisis spreading across the Atlantic by issuing a strong warning about America's failure to tackle its budget deficit.

Shares fell heavily on Wall Street on Monday after a leading ratings agency fanned fears of Europe's debt crisis spreading across the Atlantic by issuing a strong warning about America's failure to tackle its budget deficit.In a move seen by Wall Street as a "shot across the bows" of bickering politicians in Washington, Standard and Poor's (S&P) said it was cutting the outlook on the US's long-term rating from stable to negative for the first time since the attack on Pearl Harbor 70 years ago.

The announcement surprised the financial markets, where attention in recent months has been focused on the problems of the weaker nations of the eurozone. Renewed speculation that Greece will be forced to default on its debts led to a sharp sell-off in the euro, but S&P stressed that the US was not immune from the sovereign debt crisis.

In New York, the Dow Jones industrial average ended the day down 140 points, or 1.1%, with the dollar weaker on the foreign exchanges and yields rising on US treasury bills. The FTSE 100 in London was down 126 points at 5870 – a drop of more than 2% – as ongoing concerns about the eurozone's debt crisis were compounded by the setback for the world's biggest economy.

George Osborne, the chancellor, seized on the S&P warning as vindication for the coalition's stance towards deficit reduction. "S&P did the same to the UK before the election but revised us back to 'stable' following the spending review because we had a credible deficit plan," a senior Osborne aide said on Monday. He added that Labour's more cautious approach to cutting the UK's deficit was "way out of step with world opinion".

Speculation that Greece may be forced to default on its debts and a strong performance by nationalists in the Finnish election opposed to supporting the bailout of Portugal combined to send the London index down. The main stock markets in France and Germany were also down sharply on the day.

S&P said that compared with the small number of developed countries with a coveted AAA rating, the US had "very large budget deficits" which reached as high as 11% in 2009. With the political infighting between the Republicans and Democrats on the deficit now so bitter that there was a risk of the US government being shut down earlier this month, S&P said it had taken the decision to change its outlook because "the path to addressing these issues is not clear to us".

It added: "We believe there is a material risk that US policymakers might not reach an agreement on how to address medium- and long-term budgetary challenges by 2013; if an agreement is not reached and meaningful implementation is not begun by then, this would in our view render the US fiscal profile meaningfully weaker than that of peer 'AAA' sovereigns."

The White House, which last week produced proposals that would cut $4tn from the US deficit by 2022, rejected the S&P analysis. "They are saying their political judgment is that over the next two years they didn't see a political agreement" to reduce long-term deficits, Austan Goolsbee, chairman of the Council of Economic Advisers, said in an interview with Bloomberg Television. "I don't think that the S&P's political judgment is right."

While Europe has decided to make a priority of deficit reduction, the US approach has until now involved running an expansionary fiscal policy in an attempt to deliver faster growth.

Republicans have accused the Obama regime of "mortgaging the country's future", and Paul Ryan, the chairman of the House of Representatives budget committee, has come up with a more aggressive plan that would involve deep cuts in non-defence spending.

Nikola Swann, S&P's credit analyst, said: "We view President Obama's and congressman Ryan's proposals as the starting point of a process aimed at broader engagement, which could result in substantial and lasting US government fiscal consolidation. That said, we see the path to agreement as challenging because the gap between the parties remains wide. We believe there is a significant risk that congressional negotiations could result in no agreement on a medium-term fiscal strategy until after the 2012 congressional and presidential elections."

Ted Scott, director, Global Strategy at F&C, said: "The markets were caught by surprise by today's announcement at a time when analysts had been downgrading growth expectations for the US, mainly as a result of poor weather in the first quarter of 2011 and higher commodity prices.

"The downgrade is, however, only in the outlook and is unlikely to lead to a cut in the rating itself. Indeed, it should focus the mind of the politicians of all parties to agree a credible debt reduction plan now that the clock is ticking on its debt rating."

See related news :

http://analisaham.blogspot.com/2011/04/dji.html

http://analisaham.blogspot.com/search?q=bull+story

Stock to watch :

http://analisaham.blogspot.com/2011/04/tlkm.html

http://analisaham.blogspot.com/2011/04/kija.html

http://analisaham.blogspot.com/2011/04/asrijk.html

Monday, April 18, 2011

TLKM

TP : 7.800 - 8.000

Resistance : 7.350

Pattern : Falling wedges + Ascending Triangles

Beta : 0.67

Market Cap (Mil.) : Rp. 146,160,000.00

Shares Outstanding (Mil.) : 20,160.00

Annual Dividend : 288.16

Yield (%) : 3.97

Financials

P/E (TTM) : 12.36

Market Cap (Mil.) : Rp. 146,160,000.00

Shares Outstanding (Mil.) : 20,160.00

Annual Dividend : 288.16

Yield (%) : 3.97

Financials

P/E (TTM) : 12.36

EPS (TTM) : 1.79

ROI: 24.94

ROE: 27.78

Friday, April 15, 2011

ASRI

Support : 265-275

TP : 300

Beta : 1.51

Market Cap (Mil.) : Rp. 5,001,669.00

Shares Outstanding (Mil.) : 17,863.10

Annual Dividend : 1.05

Yield (%) : 0.38

P/E (TTM) : 19.59

Market Cap (Mil.) : Rp. 5,001,669.00

Shares Outstanding (Mil.) : 17,863.10

Annual Dividend : 1.05

Yield (%) : 0.38

P/E (TTM) : 19.59

EPS (TTM) : 252.13

ROI : 12.71

ROE : 12.80

Subscribe to:

Comments (Atom)